Welcome to the Sharing Economy. We now share office space where we used to have our own desk or office. We share cars using Uber or Lyft. We now are even forced to share bathrooms. In Real Estate, Time Shares have survived for many years. The new Pacaso.com offers shared equity ownership in 1st or 2nd homes. For Real Estate Investors there are many ways to share the ownership/equity or debt/loan. Today’s Blog will discuss sharing Debt on Real Estate Investments including the Pro’s and Con’s for different debt holding structures.

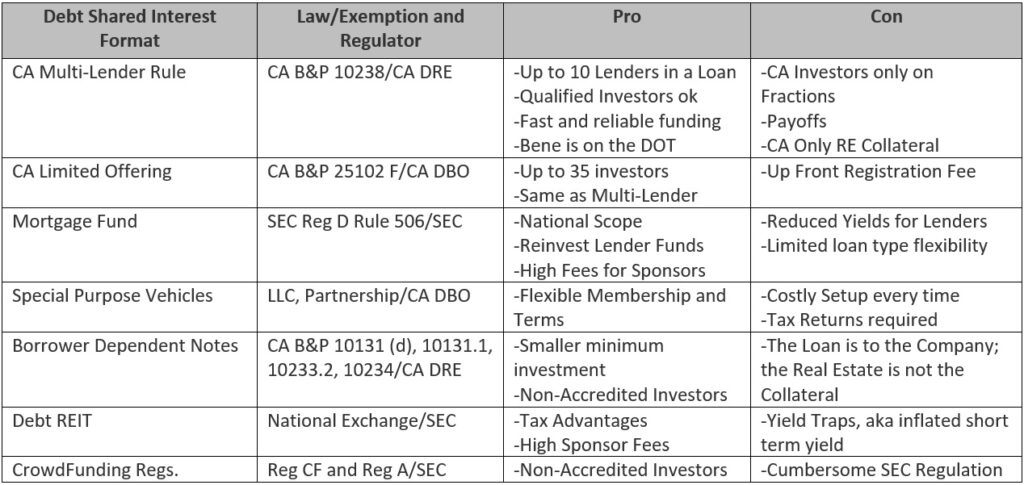

These ownership interests might be called syndicates, fractional interests, memberships, partnerships, and investment interests, but the shared interest in a real estate debt offering is consistent across the formats below:

Whether you are a Borrower or a Lender, knowing about the regulatory vehicle and/or exemption used to facilitate your investment remains critical. At Mortgage Vintage and CrowdTrustDeed (CTD), we have considered various structures, however we prefer to stick to competency in multi-lender and limited offering fractional interest models vs. a Mortgage Fund or the other options above for many reasons:

- Higher Yield – According to Armanino LLP, the average CA Mortgage Fund spins off 6.5%-7.5% yield to the Investor while CrowdTrustDeed from 2015-2020 provided a yield of 10%+ to its investors

- Loan Discretion – Lenders can pick and choose what properties to invest in with a fractional interest model. When a Lender invests in a Fund, the Lender is at the mercy of the Fund Manager to place the money and, in many cases, the Fund Manager is desperate to get those funds placed and earning interest to not dilute the Fund’s earnings and yield. This urgency to place money creates the need for higher Loan to Values (LTV’s) and riskier loans.

- Loan Maturities – Knowing the Loan Maturity allows the Lender to know when their funds may become available again for redeployment or for a Loan Extension that may keep the loan performing.

- Investment Strategy – Similar to an Investor managing a portfolio at TD Ameritrade or Schwab, our strategy at CTD has been to support the Lender that wants to build their own portfolio of Trust Deeds that are serviced at FCI Lender Services. The Lender can act as their own “Fund Manager” vs. having a Fund Manager make decisions for them.

- Control – Should a problem ever arise with a Trust Deed (TD); fractional Lenders provide more agility in resolving issues on a Reinstatement/Forbearance/Foreclosure plan.