Fix and Flip or Fix and Rent?

Deciding whether to Fix and Flip or Fix and Rent can be a difficult decision. You may be evaluating a purchase or have already put substantial work and money into renovating a property. In either case the question is; sell now, sell in a few years, refinance: which option is right for you?

By answering 5 crucial questions, you can make a wise decision about your financial real estate investment and how to move forward in the future:

- What is your core business or investment goal? Ask yourself what your short term and long term goals are for your business and this investment. If your core business is to flip properties, reinvest the proceeds and keep your construction crews working, you will want to sell quickly. If you are looking for cash flow and want a long term yield with potential capital appreciation return, a rental strategy is the best fit.

- How does the investment stack up to your yield and return objectives? If there is a big profit available from a flip due to a discounted purchase price or a value add rehab, the upfront cash offered by a Flip might be the way to go. A rental makes sense if a minor rehab, high rent and favorable loan conditions exist.

- What are your capital needs? If an upcoming large expense or additional investment requires capital, then maximize your price on the flip. If your need is current or retirement income, a rental makes sense.

- What are the maintenance and location considerations? There will be upkeep expenses of approximately 35% of the Gross Income on any property that you own. If rental income provides a positive cash flow and yield after expenses then it’s reasonable to hold onto the property until it will draw the maximum return on your investment on a sale. If those expenses begin to outweigh the potential gains, however, then it’s time to start looking for a buyer. Remember to factor in all expenses including: Insurance, property taxes, upkeep, a vacancy factor and mortgage payments.

- What are the economics around mortgage rates, housing supply, property values and rental rates?

Current Economic Arguments for a Flipping Strategy:

– Mortgage Rates are at historic lows enabling more first time and investment buyers. The average 30-year, fixed mortgage rate was 3.94 percent last week (August, 2015), according to the mortgage firm Freddie Mac. That is roughly two percentage points below the historical average.

– The increased purchase demand primarily reflects an economy operating from a stronger foundation of hiring as the recovery enters its seventh year in 2015.

– The economy has benefited from nearly 3 million new jobs in the past year (2014-2015), an influx of paychecks that has boosted the housing purchase and construction sectors.

– Home rental prices are up 4.3 percent in the past year, according to the real estate firm Zillow.Current Economic Arguments for a Rental Strategy:

– Nationally, rents have climbed 3.5% the last 12 Months (July 2014-July 2015, Source: Zillow)

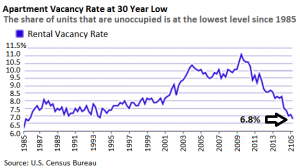

– Apartment Vacancy Rates Are the Lowest They’ve Been Since 1985

P